🏆 Excellence Award(2nd)

2024 Korea National University Statistical Competition

📌 Problem Statement

Traditional credit loan screening models often achieve reasonable predictive performance,but they suffer from a critical limitation: lack of interpretability.

In real-world financial decision-making, a model must not only predict approval or rejection, but also clearly explain why such a decision was made in order to ensure trust, fairness, and regulatory compliance.

This project addresses the question:

💡 Proposed Solution

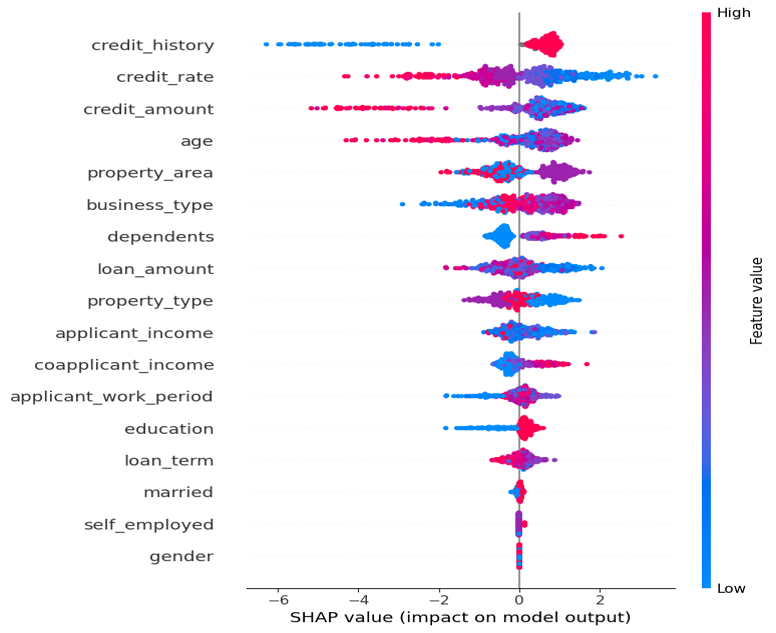

Global SHAP feature importance for credit loan screening.

Local SHAP explanation for an individual loan rejection case.

We propose an Explainable AI (xAI)-driven loan screening framework that combines:

- A high-performance machine learning model for credit approval prediction, and

- Post-hoc explainability techniques to interpret and validate the model’s decisions.

By integrating SHAP (SHapley Additive exPlanations) [1] into the pipeline, the system provides both global feature importance and individual-level decision explanations, enabling transparent and reliable credit screening . The formal SHAP equation is as follows:

\[\phi_i = \sum_{S \subseteq N \setminus \{i\}} \frac{|S|!\,(M-|S|-1)!}{M!} \Big[ f_{S \cup \{i\}}(x_{S \cup \{i\}}) - f_S(x_S) \Big]\]where

- $N$: the set of all features

- $S$: a subset of features excluding feature $i$

- $M$: the total number of features

- $f_S(x_S)$: the model prediction using only features in $S$

- $\phi_i$: the SHAP value (contribution) of feature $i$

This formula defines a fair way to distribute the model output among features by averaging each feature’s marginal contribution over all possible feature subsets.

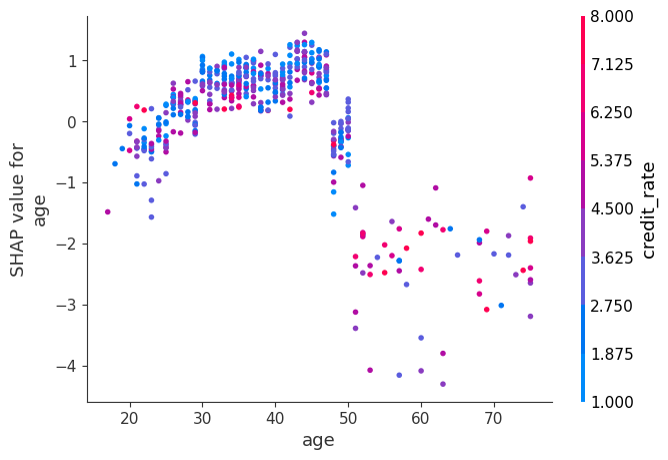

Using SHAP, we can quantitatively explain how much each variable contributes to a specific prediction.

🛠️ Technical Overview

- Dataset:

- 600 samples × 19 financial and demographic features

- Features include age, income, credit history, employment status, loan amount, and loan term

- Model:

- XGBoost classifier for loan approval prediction

- Explainability:

- SHAP used instead of simple feature importance to capture non-linear feature interactions

- Global SHAP analysis to identify dominant decision factors

- Local SHAP analysis to explain individual rejection/approval cases

- Model Refinement:

- Identified low-impact features via SHAP

- Removed the bottom 6 least-informative features

- Deployment:

- Implemented a FastAPI-based inference server

- Supports new applicant data input and returns:

- Approval/rejection decision

- Visual explanation of contributing factors

🎬 Results and Achievements

- Model Performance Improvement:

- Accuracy before feature removal: 82.11%

- Accuracy after SHAP-based feature pruning: 84.55%

- +2.44% absolute accuracy gain

- Interpretability Gains:

- Clearly identified key drivers of loan decisions (e.g., age, credit history, income stability)

- Enabled case-level explanations for rejected applicants

- Practical Impact:

- Demonstrated that xAI can be used to design efficient, transparent, and trustworthy loan screening systems

- Showed the feasibility of reducing feature complexity while improving performance

- Outcome:

- Submitted as a financial data analysis competition project

- Successfully implemented an end-to-end explainable loan screening pipeline

Commemorative Photo

📚 References

[1] S. Lundberg and S.-I. Lee,

A Unified Approach to Interpreting Model Predictions,

arXiv:1705.07874, 2017.

https://arxiv.org/abs/1705.07874